Astrology of the 1951 Treasury - Fed Accord

Between Debt and Discipline: The Battle for Control of Interest Rates, 1949–1951

Following passage of the Federal Reserve Act, the United States was drawn almost immediately into World War I, placing the newly created Federal Reserve within a system shaped by wartime finance. That pattern repeated with World War II, where the central bank again subordinated its operations to the Treasury’s borrowing needs. As a result, for much of its early history the Federal Reserve operated with only limited independence, functioning largely in support of government debt management. By the late 1940s, however, that arrangement was coming under strain, as the conditions that had justified it—war finance and emergency coordination—began to give way to the demands of a peacetime economy.

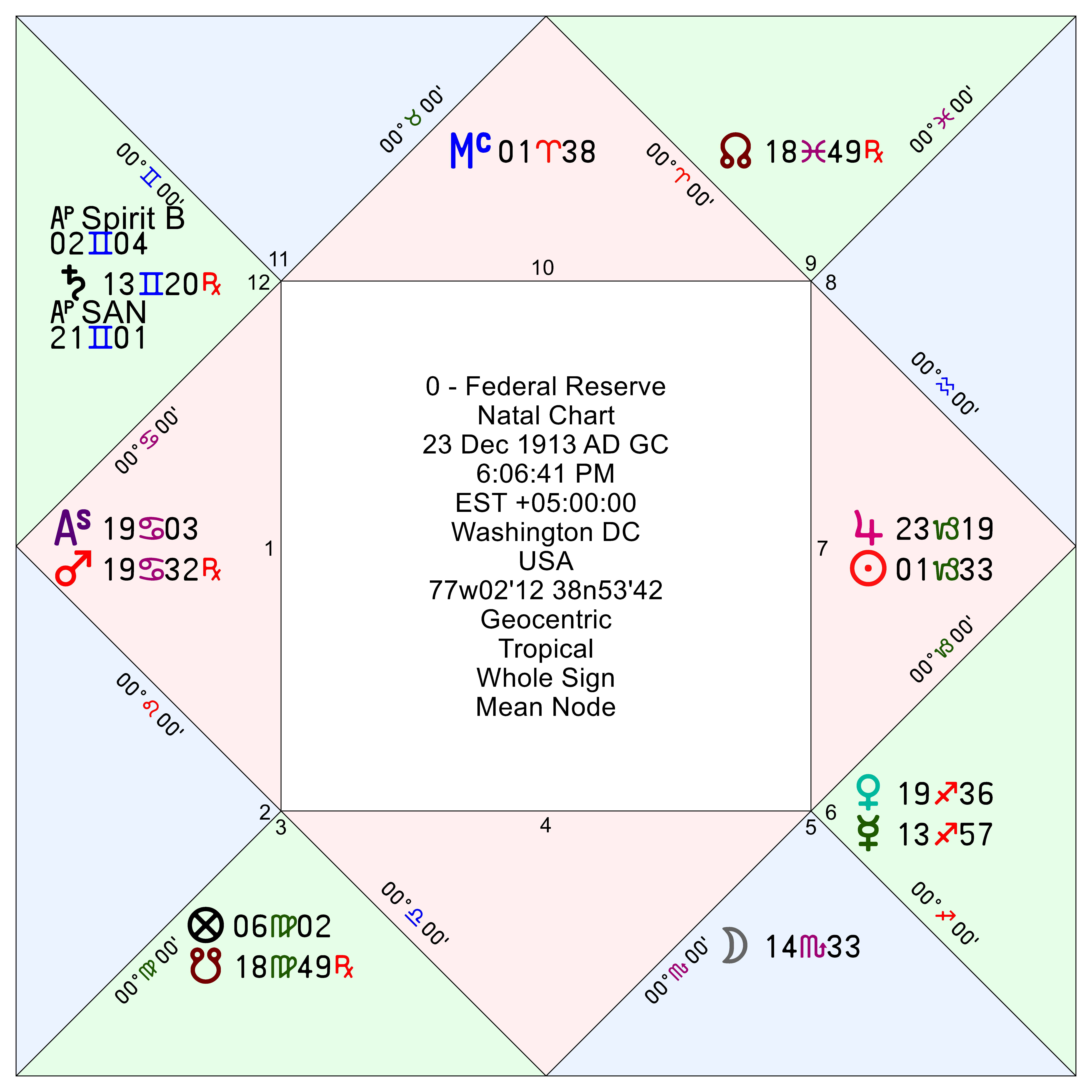

The Federal Reserve’s own horoscope describes the opposition between Fed and Treasury. At its foundation lies the Cancer–Capricorn axis, which assigns opposing roles within the credit system: Cancer signifies debtors, where borrowing is facilitated and liquidity is extended, while Capricorn signifies creditors, the holders of accumulated capital who seek discipline, structure, and reliable return on loans. In the Federal Reserve figure, that axis is placed directly on the 1st–7th house axis, anchoring the institution in the tension between debtors and creditors. With Mars in Cancer retrograde and Jupiter in Capricorn appear across that same axis, and with both planets in signs of their fall—along with Mars in retrograde motion—this is not a simple configuration to delineate. Let’s unpack it.

Mars 19CA32 – retrograde, 1st house. In direct motion, Mars in Cancer (its fall) acts defensively—protective and reactive under pressure—often shifting into a ‘rescue’ mode when activated by Moon/Scorpio through mutual reception. But in this horoscope Mars is retrograde, and for the Federal Reserve it behaves like Mars in Capricorn. In that role, Mars acts as a ‘wrecking ball,’ disrupting the Saturnian order of fixed income markets, seen in rising interest rates or widening credit spreads. Yet the mutual reception with the Moon remains strong enough to pull Mars back into its rescue function. The result is a two-stage process: Mars first destabilizes credit conditions (Capricorn phase), then reverts to its Cancer role, forcing the Fed into a protective rate-cutting response.

Bottom line: Mars/Cancer-retrograde produces lower rates as its Cancer nature seeks to defend the system—but only after its Capricorn phase has pushed markets toward stress or breakdown.

Jupiter 23CP19 – 7th house. In Capricorn (its fall), Jupiter distorts the normal functioning of debt markets, either by suppressing interest rates below market levels to facilitate government borrowing, or by tightening credit conditions in ways that burden debtors. Because Jupiter rules Mars by exaltation and bound, it becomes the primary driver of Mars’ behavior: imbalances in credit markets force Mars into a defensive posture, compelling the Federal Reserve to operate cautiously in deference to Treasury financing needs. In this role, Jupiter establishes the structural condition—distorted debt markets—that Mars must respond to, shaping the Fed’s actions during periods of financial strain.

Bottom line: Jupiter/Capricorn creates imbalances in debt markets that subordinate the Federal Reserve to Treasury priorities, forcing defensive policy responses that favor government financing over market equilibrium.

The Wartime Framework and Its Limits

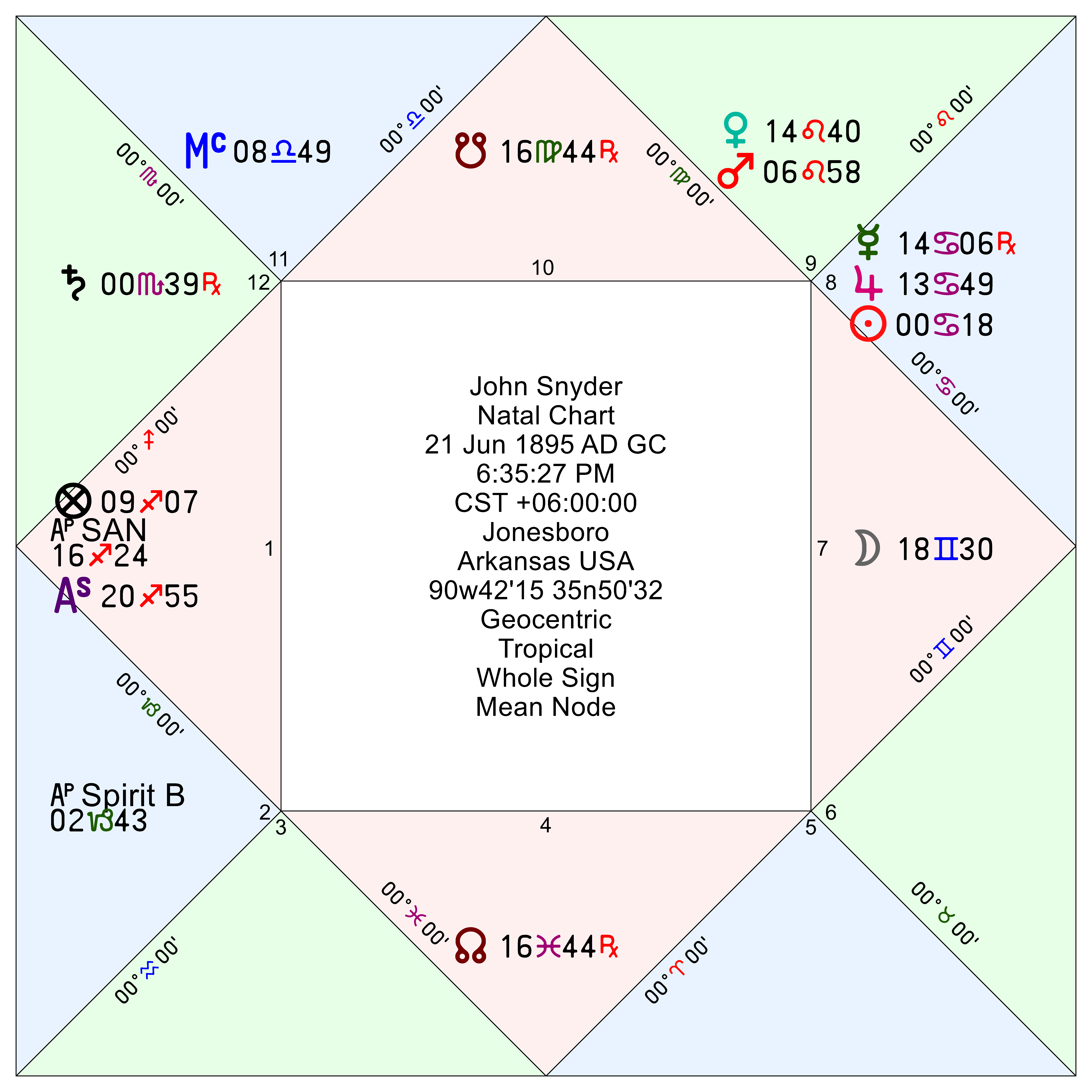

Fast forward to 1949 when postwar macroeconomic conditions normalized and it no longer made sense for the Federal Reserve to subsidize Treasury borrowing costs. At the center of the postwar conflict stood Treasury Secretary John Snyder, who maintained the low-interest-rate framework that had supported wartime borrowing and postwar stability. From Snyder’s perspective, any transition away from the status quo carried risks he was reluctant to confront too quickly. The national debt remained large, and low interest rates reduced the burden of servicing that debt while supporting credit availability across the economy. The system, in his view, still performed a stabilizing function.

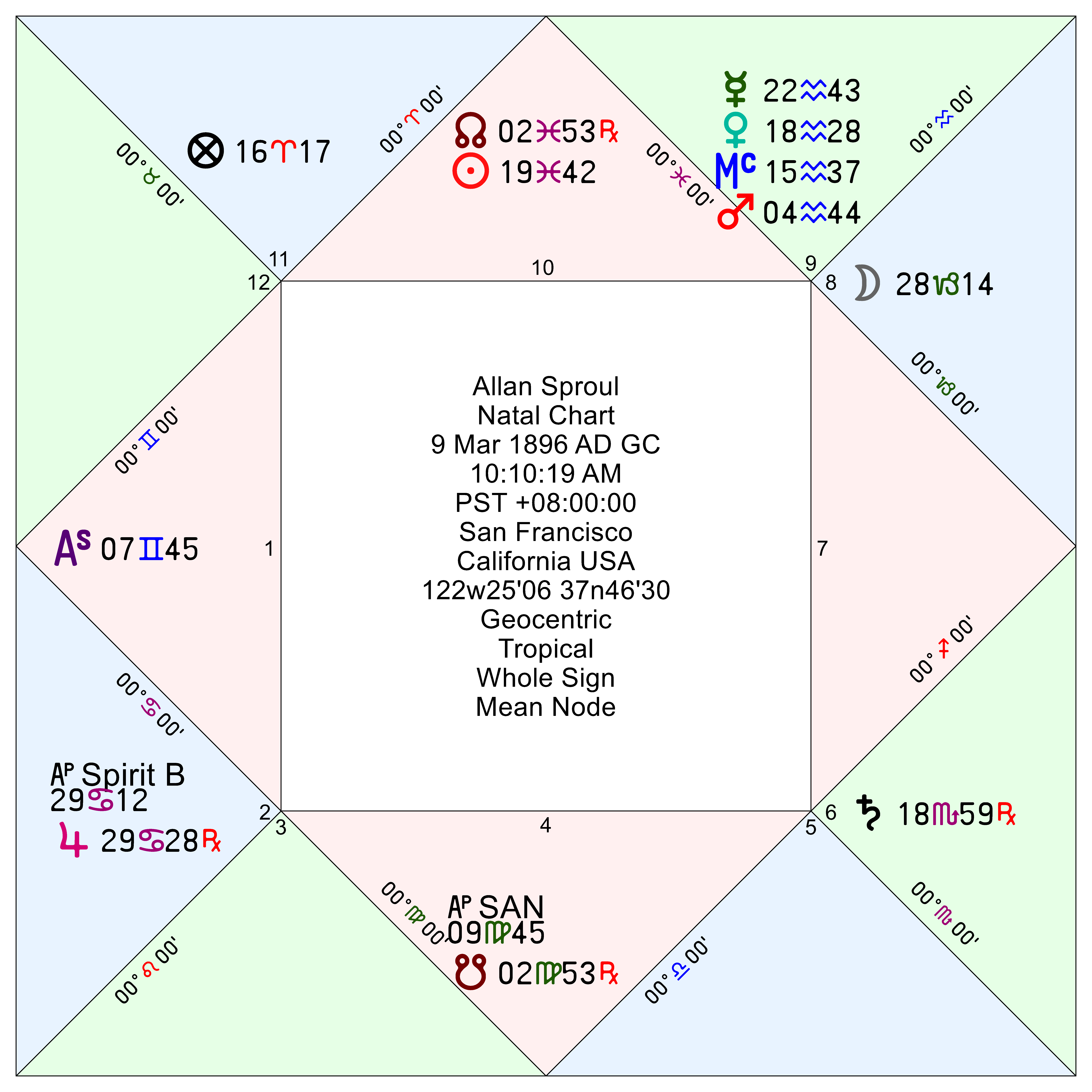

Opposing him was New York Federal Reserve President Allan Sproul, who argued that monetary policy could not remain tied to Treasury financing without limiting the Federal Reserve’s ability to respond to inflation. By 1949, the limitations of this arrangement had become more difficult to ignore. In order to maintain the rate peg, the Federal Reserve purchased government securities whenever market pressures pushed yields higher. These purchases injected liquidity into the system at moments when restraint might otherwise have been warranted. With the onset of the Korean War in 1950, inflationary pressures increased, and the contradiction became more apparent: a central bank tasked with maintaining price stability was simultaneously obligated to support a policy that could contribute to rising prices. The question was no longer whether the system had worked in the past, but whether it could continue to function under changing conditions.

Between them stood Federal Reserve Board Chairman Thomas B. McCabe, formally responsible for guiding the institution through the transition, and Marriner Eccles, who, though no longer Chairman, remained on the Board and played a visible role during the final phase of the dispute. The issue itself was straightforward but difficult in execution: whether interest rates would continue to be held down to support government borrowing or allow them to adjust in response to economic conditions.

The Federal Reserve Pushes Back

It was within this context that Allan Sproul articulated the Federal Reserve’s position with increasing clarity. His argument was not framed in abstract terms of institutional independence alone, but in practical terms of policy effectiveness. A central bank that could not allow interest rates to rise, even when inflationary pressures were building, lacked the ability to carry out its responsibilities. The issue, as he presented it, was not simply one of authority, but of function.

Thomas B. McCabe, as Chairman, occupied a more cautious position, working within the constraints of the existing arrangement while attempting to negotiate a path forward. Marriner Eccles, though no longer Chairman, provided an additional voice from within the Board—one shaped by his earlier experience during the New Deal, but now increasingly focused on the risks of inflation rather than the need for expansion. By late 1950, the Federal Reserve had begun to press more directly for a change in policy, seeking greater flexibility in its operations and relief from the obligation to maintain fixed rates.

January–February 1951: The Dispute Becomes Public

The final phase of the conflict unfolded over a matter of weeks in early 1951, as internal disagreements gave way to public confrontation. On January 25, Marriner Eccles testified before the Senate, outlining the Federal Reserve’s concerns about continued rate suppression and its inflationary consequences. This testimony placed the issue in a public forum, making it more difficult to maintain the appearance of agreement between the Treasury and the Federal Reserve.

The situation intensified following a meeting on January 31 between representatives of the White House, the Treasury, and the Federal Reserve. A White House statement suggested a common position had been reached, but Fed officials in attendance disputed that interpretation. On February 3, attendee Marriner Eccles released the Federal Reserve’s account of the meeting to the press, indicating that no such agreement had been made. This action brought the disagreement into full public view and made further delay increasingly untenable. What had been a policy dispute now carried institutional implications, with the credibility of both sides at issue.

The 1951 Accord

The Treasury–Federal Reserve Accord of 4-Mar-1951 brought the immediate conflict to a close. The system of fixed interest rate pegs was abandoned, and the Federal Reserve was no longer required to support Treasury borrowing at predetermined rates. This allowed interest rates to adjust more freely in response to market conditions and restored a measure of autonomy to the central bank’s operations.

For Snyder, the outcome marked the end of the framework he had defended. The Treasury’s ability to influence interest rate policy directly was reduced, and the emphasis shifted toward monetary control rather than debt management. For the Federal Reserve, the Accord established a different operating environment—one in which it could act with greater discretion, though still within a system shaped by practical and political constraints. The resolution reflected both a change in policy and a redefinition of institutional roles, with the Federal Reserve assuming a more independent position in the management of credit conditions.

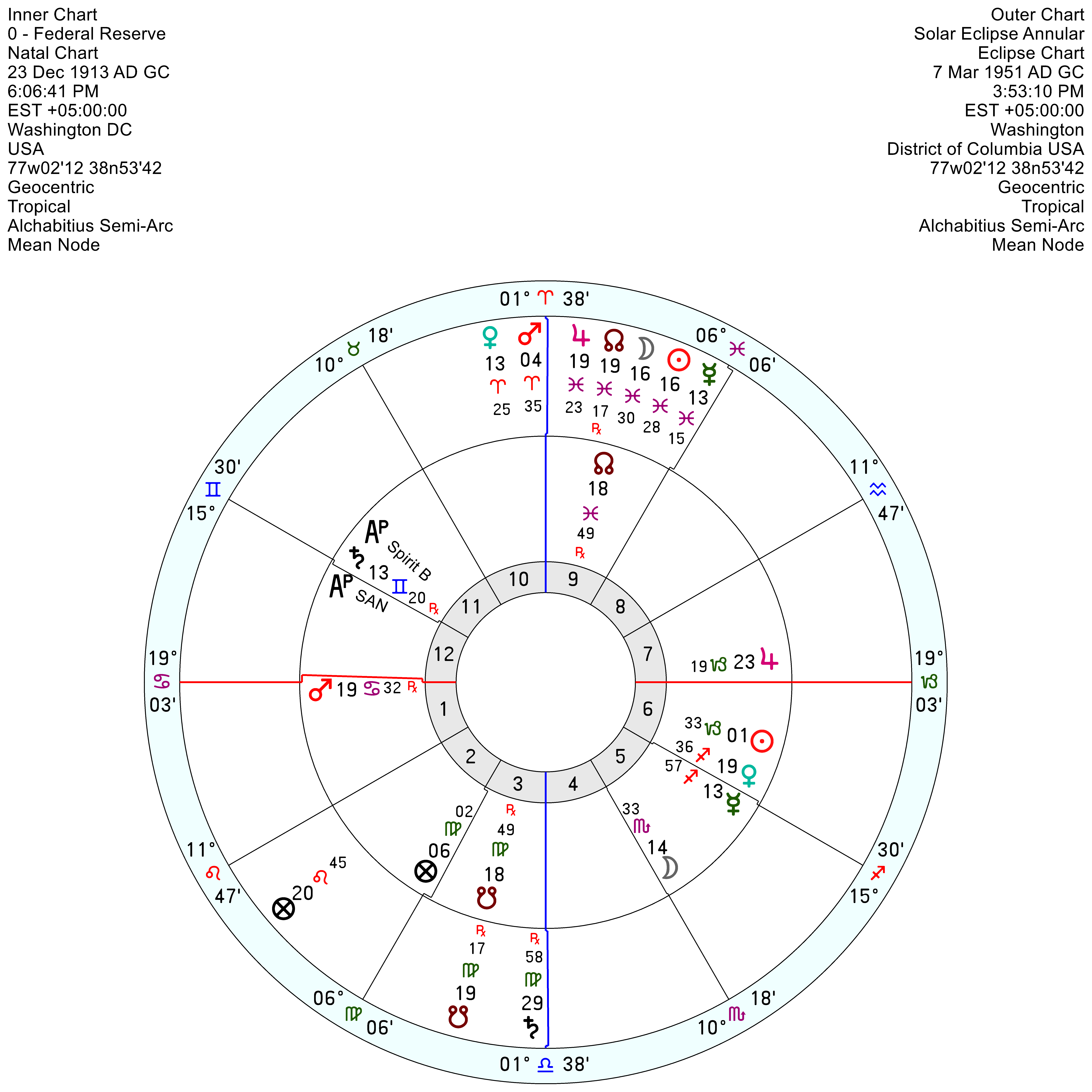

Transits. On 2-Mar-1951, a Mars-Saturn opposition perfected within one degree of the Fed horoscope’s MC/IC axis. On 3-Mar-1951 transiting Mars/Aries conjoined the MC degree. As ruler of the MC, Mars/Aries signifies the Federal Reserve reasserting control over its destiny. The following day the Treasury-Fed Accord was released on Sunday to the news media, no exact time recorded.

Eclipses. The Treasury-Fed Accord was sandwiched between a 21-Feb-1951 South Node Lunar Eclipse 2VI35 and a 7-Mar-1951 North Node Solar Eclipse 16PI30. In my opinion, the Accord is best read through the 7-Mar-1951 Solar Eclipse. But we need two more delineations to fill out this story. In addition to assigning Mars to the Fed and Jupiter to the Treasury, Mercury 13SA57 in the 6th ruling the 12th signifies inflation as a secret enemy causing the Fed and its employees’ injury. Mercury is also the bound ruler of the North Node 18PI49 with Jupiter 23CP19 the sign ruler of the North Node. With Mercury the source of inflation and Jupiter the source of distorted debt markets, both rulers amplify the North Node’s penchant for higher liquidity and inflation. Placement of the North Node in the 9th house signifies the role of the foreign lands, the courts, and the judiciary where the North Node effects occur.

And so for the 7-Mar-1951 solar eclipse:

Mars 4AR35 in its sign of rulership signifies the Fed in control of its destiny.

Mars 4AR35 is also in the bound of Jupiter/Aries

Jupiter 19PI23 in its sign of rulership a degree past the North Node signifies increased liquidity.

Jupiter 19PI23 is also in the bound of Mars/Pisces

Both Mars and Jupiter in each other’s bounds meets the technical condition of generosity by bound which links the two planets and creates the agreement.

Mars and Jupiter are also widely conjunct by antiscia which has a similar effect as generosity.

North Node 19PI17 is in the bound of Mars, unlike its natal position 18PI48 in Mercury’s bounds.

Mercury 13PI15 is in both the sign and bound of Jupiter.

Bottom Line: Mars and Jupiter in their own signs are linked by generosity and create the agreeement. Mars/Aries angular in the 10th house and conjunct the MC degree is the stronger of the two and has the final say. With Jupiter ruling Mercury, inflation is contained because the Treasury (Jupiter) now allows the Fed (Mars) to raise interest rates if necessary.

The Federal Reserve moved away from a framework centered on supporting Treasury borrowing toward one in which it could adjust policy in response to economic conditions. At the same time, the underlying tension between fiscal needs and monetary objectives did not disappear. It remained present, but within a different institutional arrangement—one that placed greater responsibility on the Federal Reserve to manage the balance between expansion and restraint.

After the Accord: A Qualified Settlement

The settlement reached in 1951 did not resolve all internal differences within the Federal Reserve. In the period that followed, the institution adopted a “bills only” approach, limiting open market operations to short-term Treasury securities. This represented a cautious interpretation of its newly regained independence, emphasizing restraint and minimizing direct intervention in longer-term markets.

Allan Sproul disagreed with this limitation. For him, the ability to operate across the full range of maturities was an essential component of effective monetary policy. Restricting operations to Treasury bills reduced the Federal Reserve’s capacity to influence broader credit conditions, leaving part of the system beyond its immediate reach. This disagreement over operational scope contributed to his resignation, underscoring that while the question of independence had been addressed, the question of how that independence would be exercised remained unsettled.

Now meet the players behind the Treasury-Federal Reserve Accord of 1951.

Click on each name for the natal database entry which includes biography and astrological models for the victor, physiognomy, Moon’s Configuration, Influence of Sect, and the Early/Late Bloomer thesis.

Snyder’s natal North Node 16PI44, like the Fed’s North Node 18PI49, is in the bound of Mercury/Pisces. The Treasury-Fed accord marks a nodal return for both horoscopes. For Snyder, at also marks a return of the South Node in the 10th which signifies diminished career and reputation. This is one reason by Snyder lost the battle between the Treasury and the Federal Reserve.

Sproul’s Sun 19PI42 is closely conjunct the Fed’s North Node though in the bound of Mars, not Mercury. This makes the 7-Mar-1951 solar eclipse a better match to Sproul’s horoscope, not Snyder’s or the Fed’s. In addition, the preceding 21-Feb-1951 lunar eclipse was conjunct Sproul’s South Node.

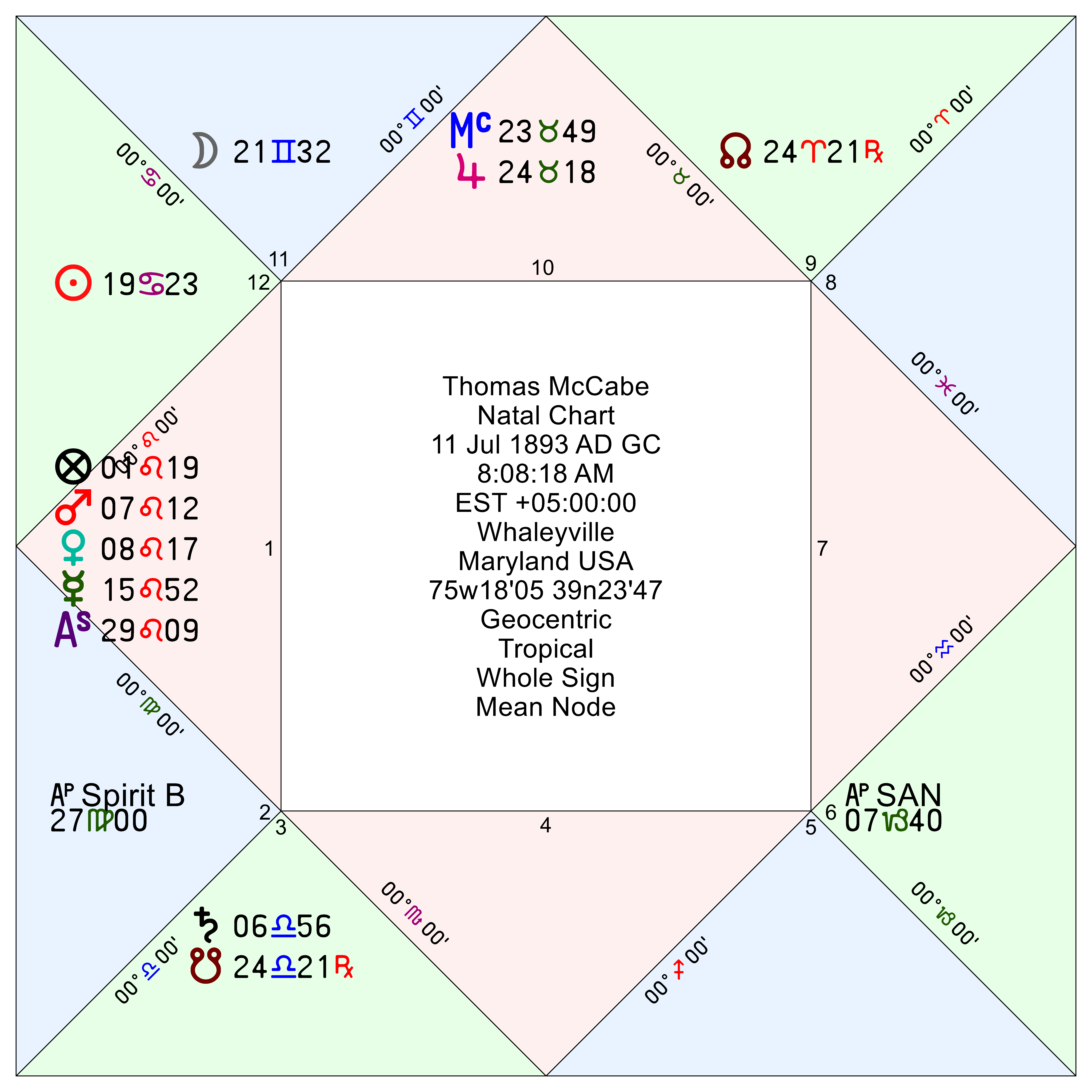

The least connected of these three actors in the 1951 Accord, McCabe is nevertheless connected to the Federal Reserve horoscope through his Sun 19CA23 conjunct the Fed’s Mars 19CA32. This synastry confirms Mars’ rulership of the 10th house in the Fed horoscope as the Fed Chair directly; here, Thomas McCabe.