Astrology of the early Federal Reserve: 1913-1933

A Central Bank Without a Playbook: War Finance, Real Bills, and the Struggle for Control

The founding of the Federal Reserve in 1913 is often treated as the birth of a modern central bank. But in reality, the institution began as something far more tentative—an incomplete framework shaped as much by personalities and circumstance as by statute. The Federal Reserve Act itself, at roughly thirty pages, established a system of regional banks and a governing board, yet left vast areas of monetary practice undefined. In astrological terms, this was an institution born under conditions that emphasized potential over prescription—a chart with structure, but little operational determinism.

Just as important, the early Federal Reserve was not independent. The boundary between the Treasury and the Fed—so central to modern monetary policy—barely existed. Within a year of Woodrow Wilson signing the Act, the outbreak of World War I transformed American finance. The Treasury’s immediate priority became the financing of war through Liberty Bond campaigns, and this imperative quickly subordinated the Federal Reserve to fiscal needs. The chart of the institution, so to speak, was immediately activated under martial conditions: Mars themes of war finance, debt issuance, and national mobilization overtook any theoretical commitment to neutral monetary governance.

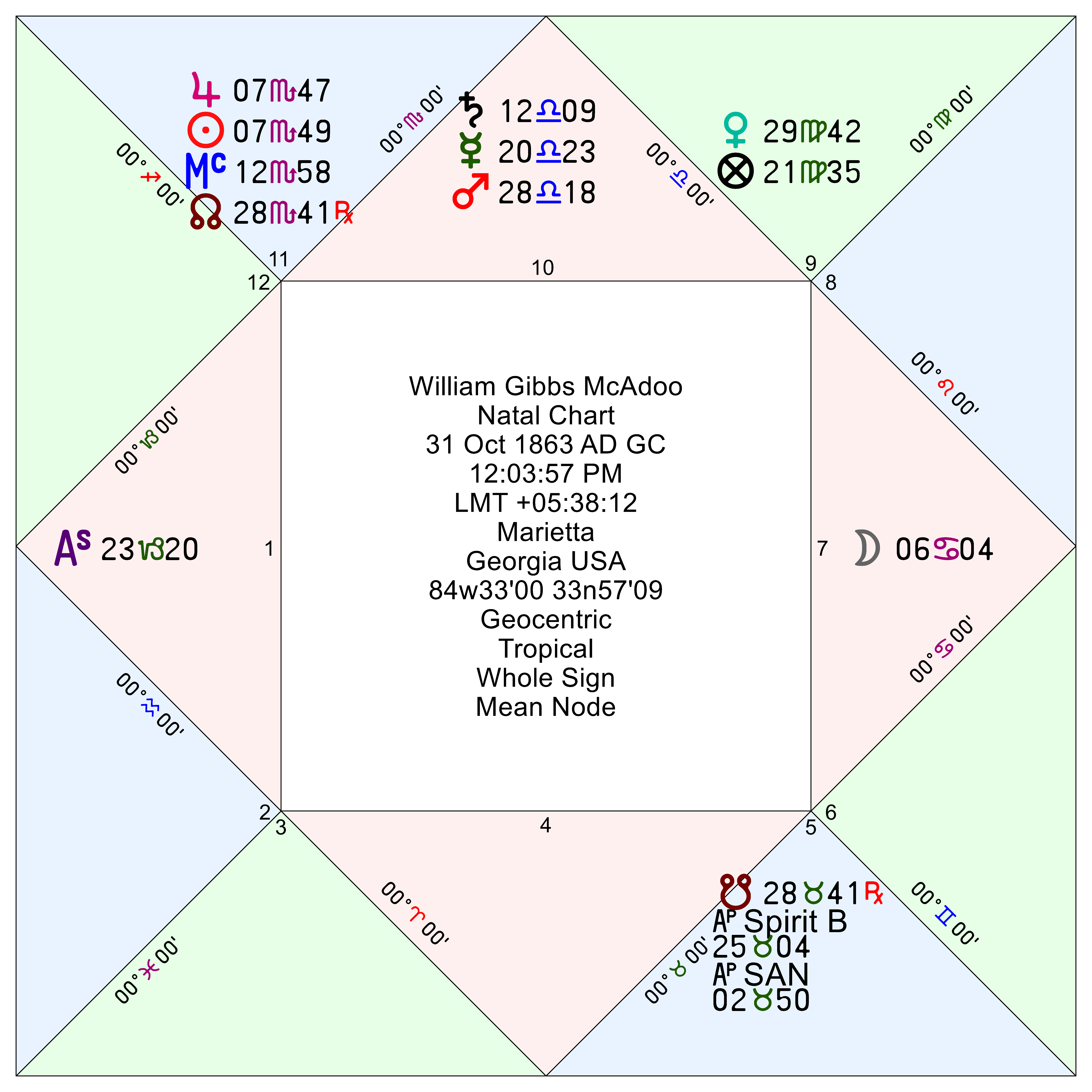

No figure embodied this shift more effectively than Treasury Secretary William Gibbs McAdoo, who rose to the occasion by organizing massive bond drives that channeled public savings into the war effort. In doing so, McAdoo effectively positioned the Treasury—not the Federal Reserve—as the commanding force in American financial policy. The Fed, still in its infancy, functioned as a supporting mechanism, providing liquidity and stability to a system whose primary objective was wartime funding rather than peacetime equilibrium.

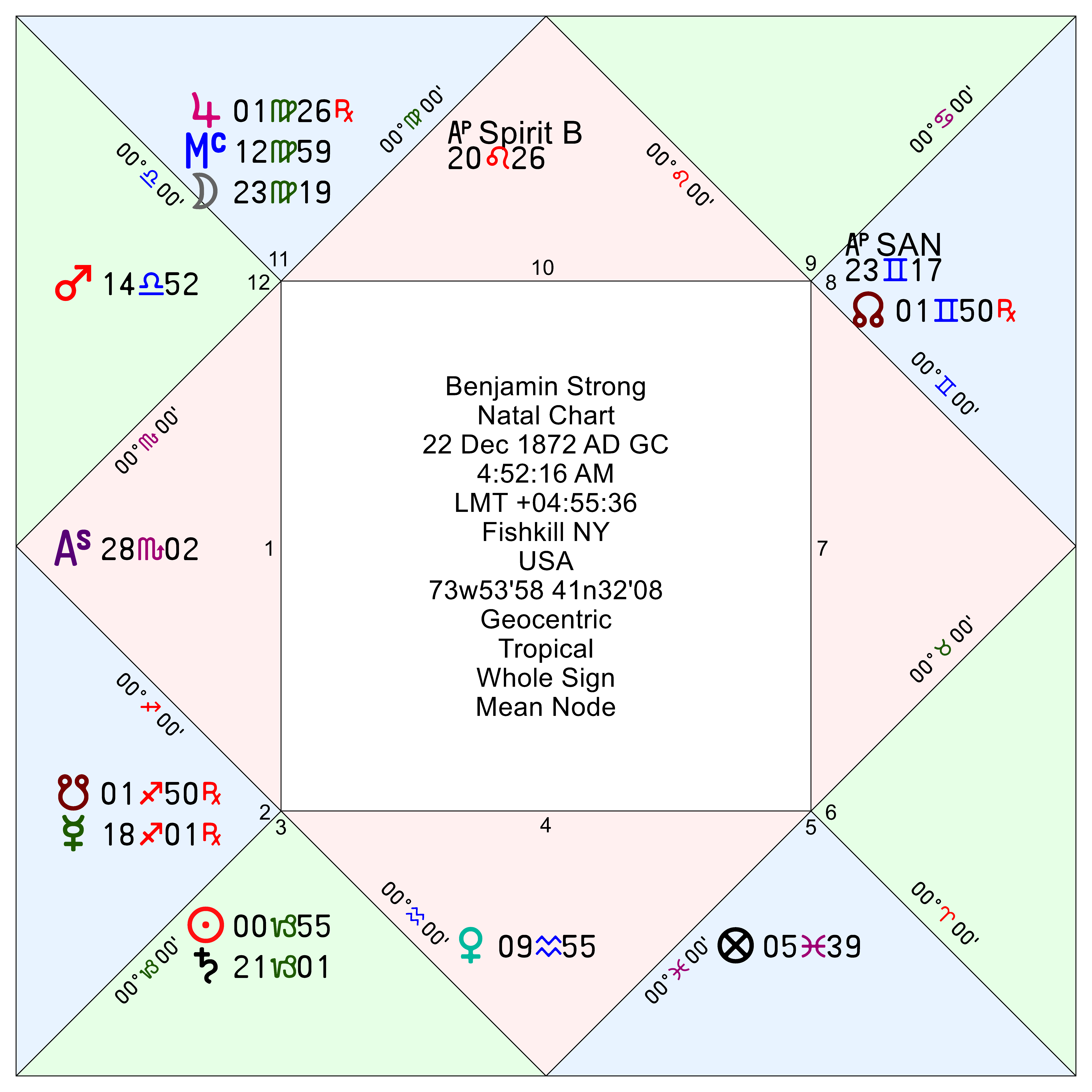

Meanwhile, the Federal Reserve Board in Washington lacked strong leadership, and functional authority drifted elsewhere. It was at the Federal Reserve Bank of New York, under Benjamin Strong, that the institution began to take on a more coherent identity. Strong extended the Fed’s role in maintaining an “elastic currency”—a key objective of the Act—through adherence to the real bills doctrine, which held that money supply should expand and contract in response to short-term commercial needs. In practice, this meant discounting self-liquidating commercial paper, tying the supply of money to the rhythms of trade.

Yet in executing this doctrine, Strong and the New York Fed stumbled upon something far more consequential: the ability to influence the money supply through open market operations. By buying and selling government securities, the Fed could add or withdraw reserves from the banking system—effectively creating or destroying money. What began as a technical adjustment mechanism evolved into the central tool of modern monetary policy. This was not a fully theorized breakthrough, but rather an accidental discovery, emerging from practice rather than design—an outcome entirely consistent with an institution whose founding document left so much unsaid.

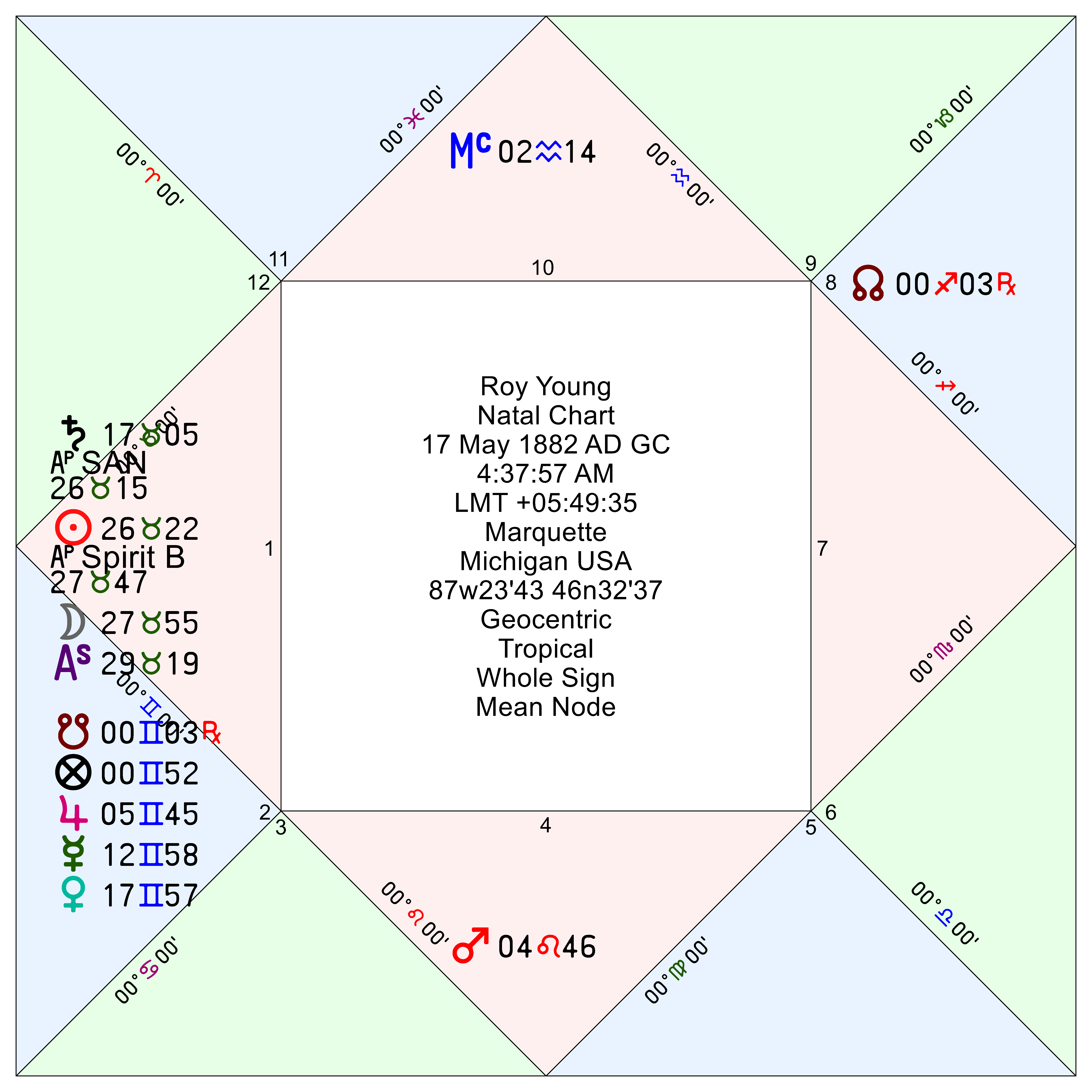

Strong’s influence became so dominant that the first six Washington-based Governors of the Federal Reserve Board are often omitted in early Fed histories. They were Charles S. Hamlin (1914-1916), W. P. G. Harding (1916-1922), Daniel R. Crissinger (1923-1927), Roy A. Young (1927-1930), Eugene Meyer (1930-1933), and Eugene R. Black (1933-1934). For the Regulus LLC natal database, I include both Roy Young and Eugene Meyer who sat as Governors following Benjamin Strong’s death in 1928. Both Young and Meyer proved unable to articulate or implement a coherent response to the gathering economic crisis. Lacking a philosophical foundation for intervention, they presided over a Federal Reserve that failed to counteract the deflationary spiral of the Great Depression.

At the same time, Treasury Secretary Andrew Mellon exerted a powerful but ultimately destructive influence. Mellon’s adherence to liquidationist principles—allowing failing firms to collapse and excesses to purge themselves—aligned with the prevailing passivity of the Federal Reserve. Rather than offsetting contraction, policy reinforced it. The combined effect was a deepening of the Depression, as both institutions failed to recognize—or act upon—the tools that had been quietly developed in the preceding decade.

From an astrological perspective, the period from 1913 to 1933 reveals an institution struggling to integrate its own capacities. The early Federal Reserve possessed the mechanisms of monetary control but lacked the philosophical and administrative coherence to deploy them effectively. Authority oscillated between Treasury dominance and New York innovation, without a stable center. The result was a system capable of elasticity in theory, but rigidity in crisis.

This formative era ended not with gradual evolution, but with systemic failure. Only with the arrival of a new leadership constellation—with Marriner Eccles at the Federal Reserve willing to battle Henry Morgenthau Jr. at the Treasury, under Franklin Roosevelt—did the balance shift toward a more interventionist and coordinated monetary regime. The lessons of the earlier period would be absorbed, but only after profound economic collapse.

What follows in this series is a closer examination of the five central figures who shaped this early history: McAdoo, Strong, Young, Meyer, and Mellon. Each represents a distinct expression of the unresolved tensions within the Federal Reserve’s founding chart between independence and subordination.