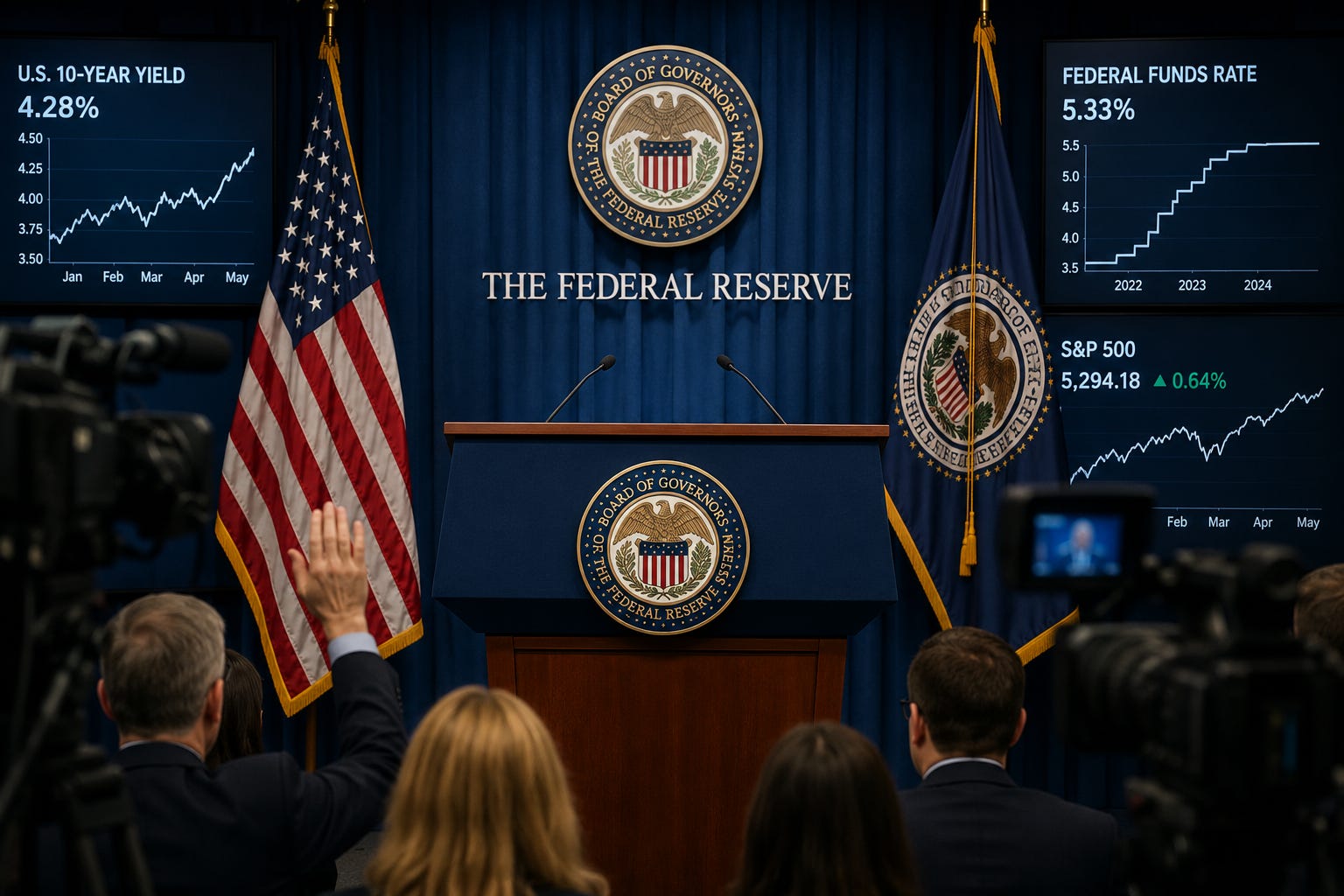

Astrology of the Federal Reserve (2006-2026)

From central bank mystique to permanent crisis management

The transition from the Volcker-Greenspan era to the Bernanke-Yellen-Powell era marked one of the most important institutional transformations in the history of the Federal Reserve. During the 1980s and 1990s, Paul Volcker and Alan Greenspan governed through a combination of interest rate policy, institutional distance, and strategic ambiguity. Volcker restored the credibility of the dollar through forceful anti-inflation policy while Greenspan cultivated a style of deliberate opacity in which markets attempted to decipher hidden meanings from carefully worded testimony. By the time Ben Bernanke assumed office in 2006, however, the Federal Reserve confronted a radically different environment shaped by globalization, financialization, excessive leverage, and mounting systemic fragility inside the banking system.

The Bernanke-Yellen-Powell era transformed communication itself into an instrument of monetary policy. Under Bernanke the Federal Reserve greatly expanded its use of press conferences, policy projections, and forward guidance in an effort to stabilize expectations during the Great Financial Crisis. Janet Yellen continued this framework through a cautious and highly transparent approach centered on labor market conditions and gradual normalization of interest rates. Jerome Powell further expanded the public role of the Federal Reserve through frequent media appearances and direct communication during periods of financial stress. Unlike the Greenspan era, in which uncertainty itself reinforced the mystique of central banking authority, the post-2008 Federal Reserve increasingly attempted to guide markets through continuous explanation and reassurance. Monetary policy became not merely a question of interest rates, but of managing confidence, expectations, and investor psychology.

The Federal Reserve also evolved into a permanent crisis-management institution during the twenty years following 2006. Bernanke established the framework for emergency liquidity facilities, quantitative easing, and large-scale intervention in financial markets during the collapse of 2008-2009. Yellen preserved this post-crisis architecture while attempting to maintain economic expansion without destabilizing markets dependent upon low interest rates and abundant liquidity. Powell ultimately expanded these interventionist policies to unprecedented levels during the COVID crisis, when the Federal Reserve effectively acted as the central stabilizing institution of the American financial system. By the end of Powell’s first term, the Federal Reserve no longer functioned simply as a manager of inflation and employment, but as a permanent guardian of systemic financial confidence in an era increasingly defined by recurring economic and market disruptions.

Ben Bernanke served as the principal architect of the post-2008 Federal Reserve order. A scholar of the Great Depression before becoming Federal Reserve Chair, Bernanke approached the financial crisis through the lens of systemic collapse and the dangers of deflationary contraction. Under his leadership the Federal Reserve introduced emergency lending facilities, quantitative easing, large-scale asset purchases, and forward guidance on an unprecedented scale while simultaneously transforming public communications into a central component of monetary policy itself. Bernanke’s tenure permanently altered the size, scope, and visibility of the Federal Reserve, shifting the institution away from the comparatively restrained and opaque style of the Greenspan years toward a far more interventionist and publicly engaged model of central banking. In historical terms, Bernanke represented the decisive transition from the old postwar Federal Reserve framework into the era of permanent monetary stabilization and financial crisis management.

Janet Yellen largely consolidated and stabilized the institutional framework created under Bernanke rather than attempting to fundamentally reinvent it. Her tenure focused upon maintaining economic expansion, supporting labor market recovery, and carefully managing the difficult process of monetary normalization after years of near-zero interest rates. Yellen governed through gradualism and caution, repeatedly emphasizing the dangers of tightening policy too quickly in an environment still shaped by weak inflation and lingering post-crisis fragility. Unlike Volcker’s willingness to shock markets through abrupt policy changes, Yellen favored predictability, transparency, and incremental adjustment designed to reassure both investors and the broader economy. In this respect her tenure represented the maturation of the post-2008 Federal Reserve system: a central bank increasingly committed not only to controlling inflation, but also to sustaining financial stability and preventing disruptions to an economic expansion heavily dependent upon accommodative monetary conditions.

Jerome Powell inherited the Bernanke-Yellen framework as the first non-academic Federal Reserve Chair since G. William Miller, bringing a background rooted more in law, government, and financial markets than in theoretical economics. Initially expected to continue the gradual normalization policies of the late Yellen years, Powell instead confronted two of the most disruptive economic crises in modern American history: the COVID pandemic and the inflationary aftermath that followed. Under Powell the Federal Reserve expanded emergency intervention to levels far beyond even the 2008 response, deploying massive liquidity programs and stabilizing financial markets during a period of extraordinary uncertainty and economic shutdown. Powell also became the most publicly visible Federal Reserve Chair since the institution’s founding, relying upon direct communication and frequent public appearances to calm markets and shape expectations during periods of instability. Yet his later struggle against post-pandemic inflation simultaneously revealed both the power and the limitations of the post-2008 Federal Reserve order created under Bernanke, forcing the institution back toward a more openly restrictive policy stance reminiscent of earlier inflation-fighting eras while operating within a vastly larger and more interventionist financial system.

Now meet the Fed Chairs that wrote the latest chapter of Fed History.