Astrology of The Federal Reserve: 1951–1978

From the Treasury-Federal Reserve Accord to the Great Inflation

The modern history of the Federal Reserve begins, in many respects, with the Treasury-Federal Reserve Accord of 1951. This agreement freed the Fed from the obligation to support Treasury bond prices and marked the restoration of central bank independence after the financial repression of World War II. It is also the natural starting point for Allan Meltzer’s second volume of A History of the Federal Reserve, which carries the story forward through 1969.

But the story does not end there. In fact, it is only just beginning.

The final years of the William McChesney Martin era and the full tenure of Arthur F. Burns belong to a single, continuous chapter: the rise of the Great Inflation of the 1970s. To understand that inflation—and why it proved so difficult to control—we must extend the narrative beyond Meltzer’s endpoint and follow the institutional breakdown through 1978, when the limits of the Burns Fed became fully visible.

This period is best understood not as a sequence of isolated policy errors, but as a transition from discipline to accommodation, unfolding across three figures who occupied different parts of the system: Martin at the Fed, Burns at the Fed, and John Connally at Treasury.

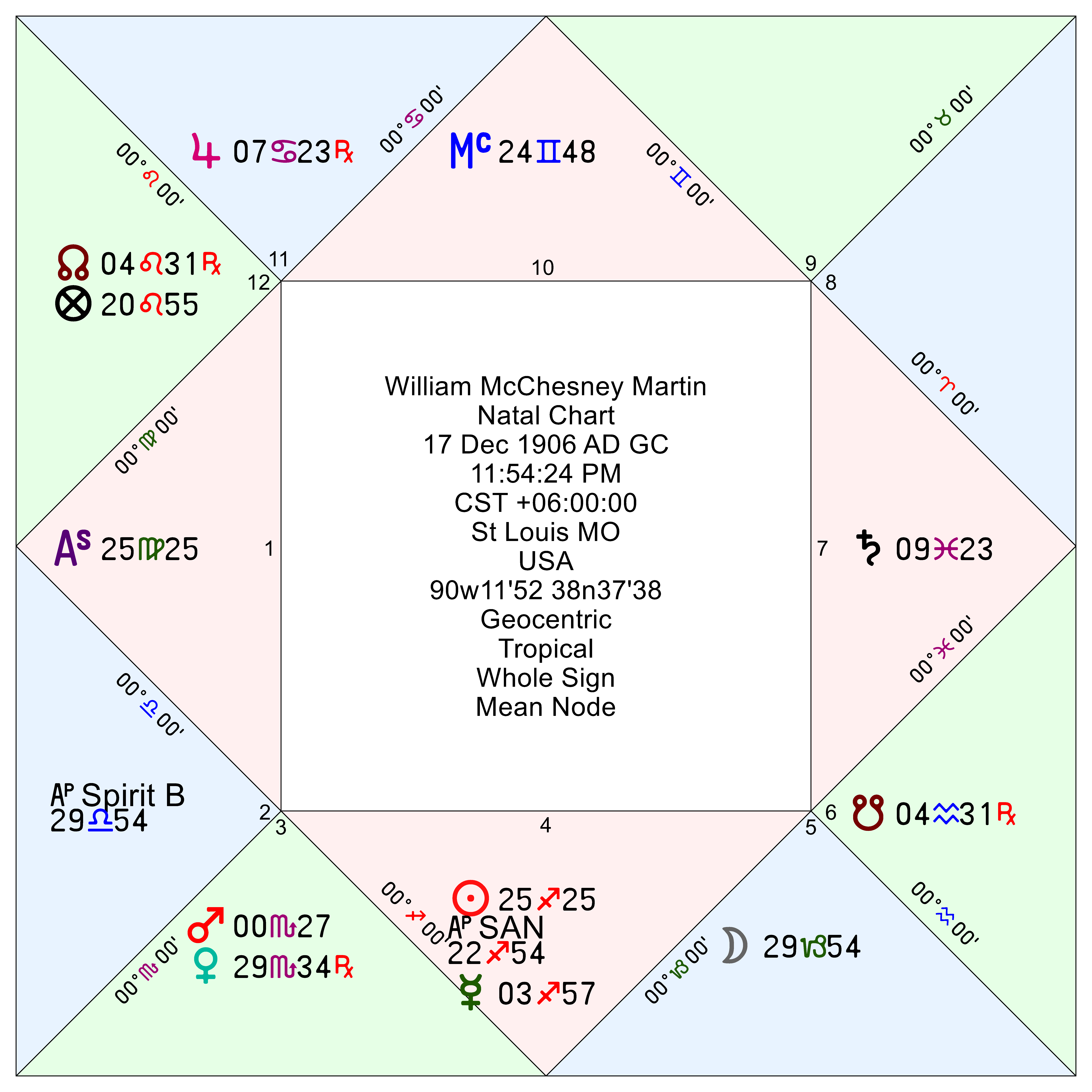

William McChesney Martin — Discipline Under Pressure

Martin’s long tenure (1951–1970) established the post-Accord Federal Reserve as a credible guardian of price stability. His famous dictum made during a 19-Oct-1955 speech before a group of New York investment bankers—“The Federal Reserve…is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up”—captures both the spirit and the difficulty of the role. For much of the 1950s and early 1960s, Martin succeeded. Inflation remained contained, and the Fed demonstrated a willingness to tighten policy when necessary, even at the cost of short-term discomfort.

Yet the system began to strain in the mid-1960s. The escalation of Vietnam War spending and the expansion of Great Society programs placed increasing pressure on monetary policy. The turning point is often captured in Martin’s confrontation with Lyndon B. Johnson, who famously “took him to the woodshed” in 1965 after a rate increase. From that point forward, the balance shifted. Between roughly 1966 and 1970, the Fed’s commitment to restraint weakened, policy became more equivocal, and inflationary pressures began to build.

In the framework developed in the Natal Database entry for Martin, this loss of control is not accidental. It coincides with the activation of Mercury in Sagittarius—a significator of price inflation—first by the Moon’s application and second as Major Firdaria Ruler from 1968-1981 which accurately times the 1970s Great Inflation.

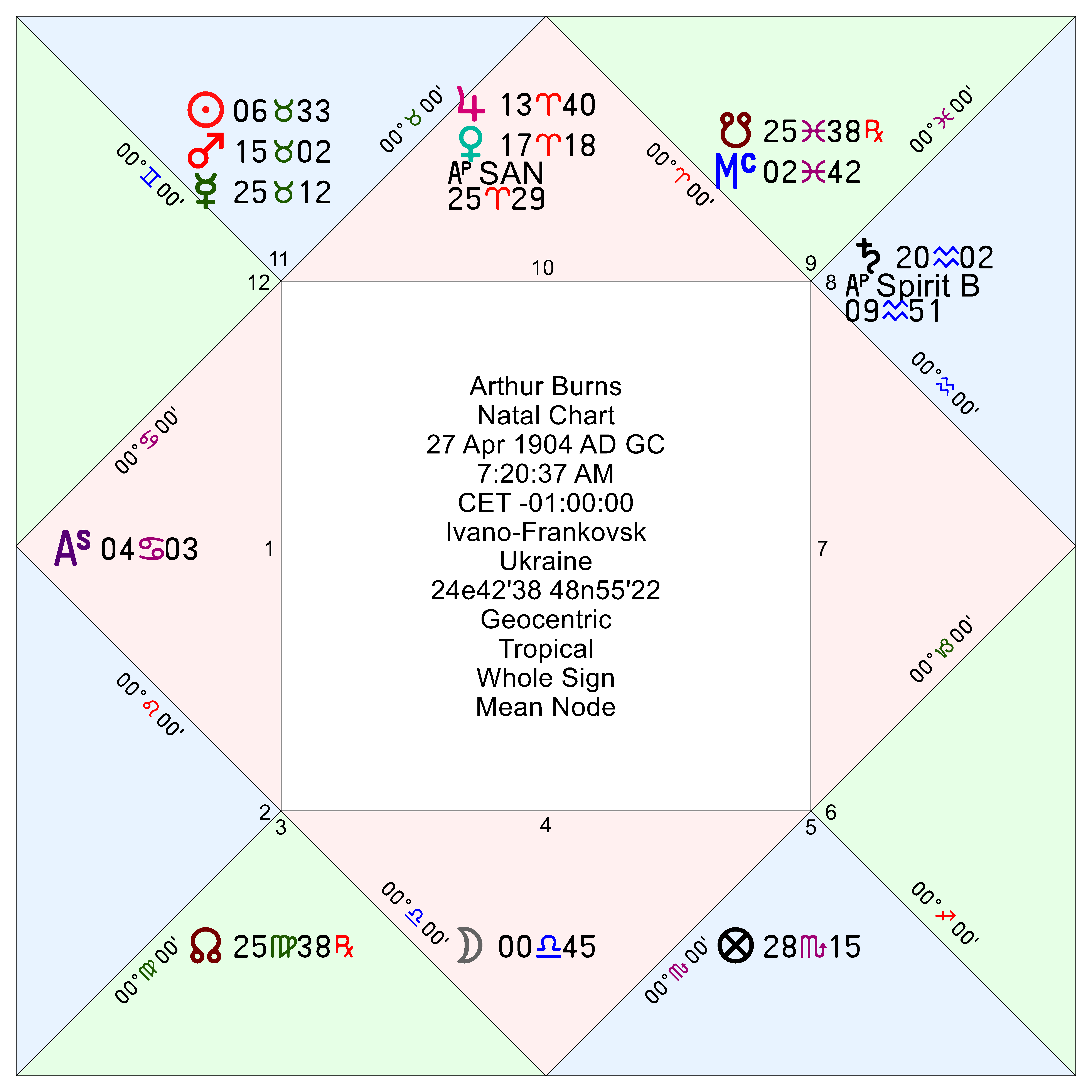

Arthur Burns — Managing the Cycle, Not the Money

When Arthur Burns assumes the chairmanship in 1970, he inherits a system already in motion. Inflation is rising, credibility is eroding, and the external discipline of the Bretton Woods system is under increasing strain. Burns does not initiate the Great Inflation, but he presides over its decisive expansion.

His approach reflects his intellectual formation. Trained under Wesley Clair Mitchell and shaped by his leadership at the National Bureau of Economic Research, Burns views the economy through the lens of business cycles and institutional behavior, not through monetary aggregates. Inflation, in his framework, is driven by wage pressures, administered prices, and structural rigidities. The solution, therefore, lies not in aggressive monetary tightening, but in administrative control—most notably wage and price controls.

As the Natal Database entry for Burns makes clear, this framework leads to a critical fragmentation: inflation is treated as a series of discrete problems rather than a unified monetary process. Policy follows accordingly. Interest rates are held too low in the early 1970s, monetary growth accelerates, and inflation becomes embedded in the system. Controls delay the adjustment, but do not prevent it. When they fail—as they do decisively by 1974—the underlying forces reassert themselves with greater intensity.

Burns’ tenure thus represents a shift in the Fed’s role. No longer the institution that removes the punchbowl, the Fed becomes an institution that tries to manage the party while it continues, with predictable results.

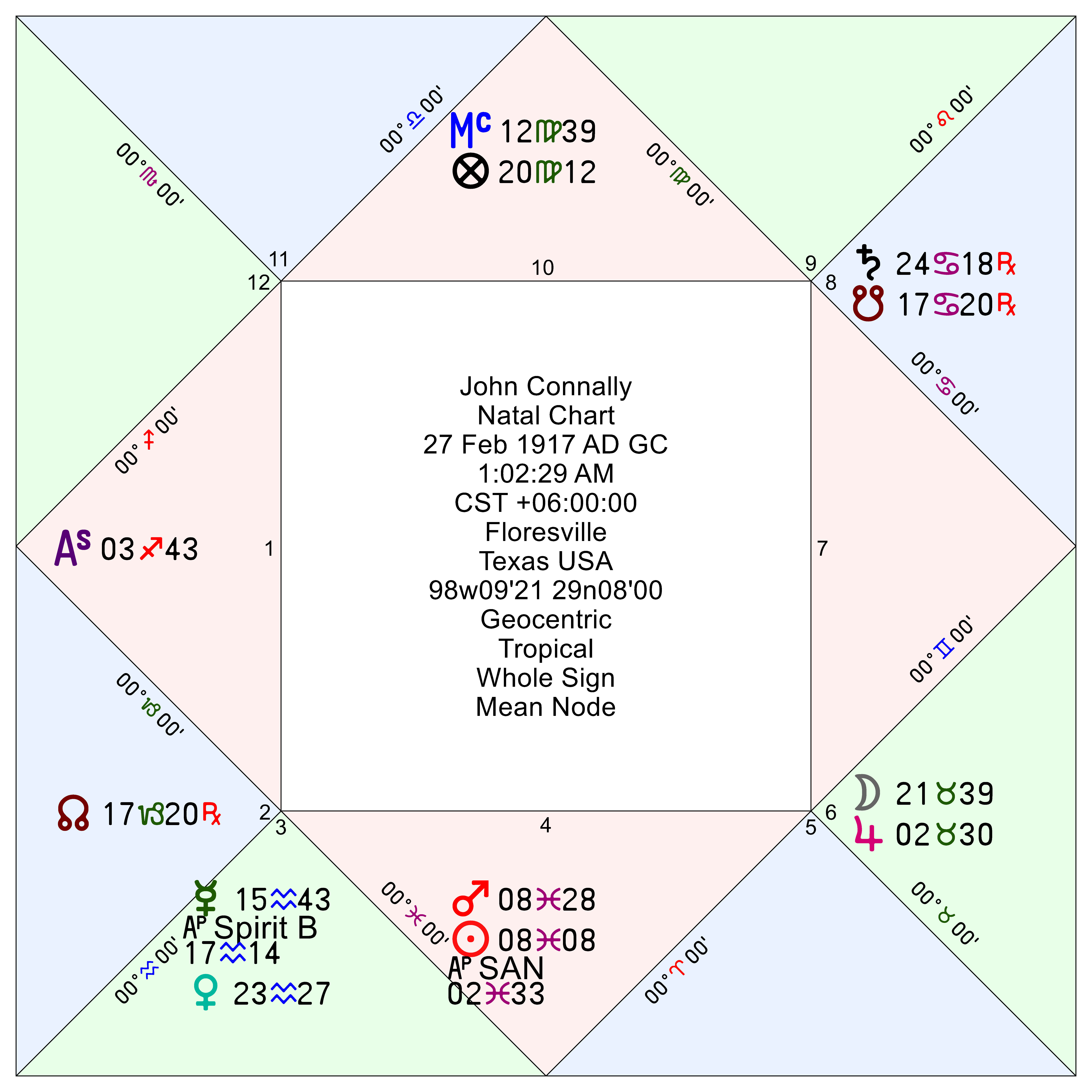

John Connally — Breaking the System

If Martin represents frayed discipline and Burns represents accommodation, Connally represents rupture.

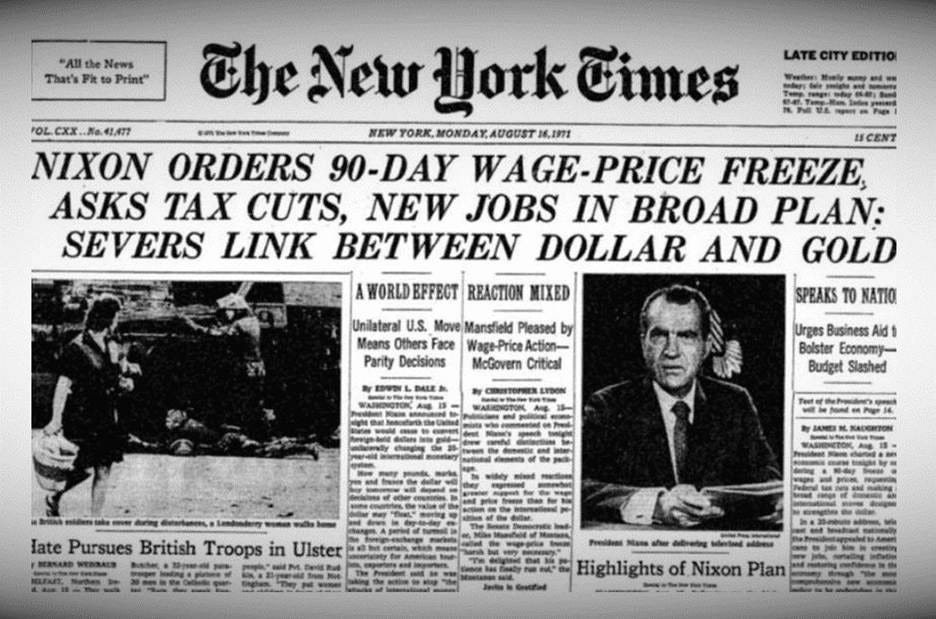

Serving as Treasury Secretary from 1971 to 1972, Connally plays a decisive role in one of the most important macroeconomic events of the twentieth century: the Nixon Shock of August 15, 1971. In a single weekend, the United States:

suspends gold convertibility

imposes wage and price controls

restructures the international monetary system

The consequences are profound. The gold window—long the external constraint on U.S. monetary policy—is closed. The dollar is no longer anchored to gold. The system shifts from fixed exchange rates to a more fluid, politically managed regime.

As the Connally Natal Database entry shows, this was not merely a technical adjustment, but a reordering of value itself. Connally’s approach is pragmatic and forceful: the system is no longer sustainable, so it must be broken. His famous remark—“the dollar is our currency, but your problem”—captures the shift from cooperation to assertion.

The timing is critical. Burns’ monetary policy has already weakened the structure. Connally’s actions remove the final external constraint. The combination transforms a developing inflation problem into a full systemic break, accelerating the transition to the inflationary regime of the 1970s.

A System in Transition

Taken together, these three figures describe a coherent progression:

Martin establishes discipline, then loses it under political pressure

Burns inherits the system and attempts to manage it through control rather than restraint

Connally removes the external constraints, allowing the system to expand freely

The result is not a single policy mistake, but a structural transition in how the U.S. economy is governed. The Federal Reserve moves from an institution capable of restraining inflation to one that accommodates it, while the international monetary system shifts from fixed rules to political management.

By the mid-1970s, the consequences are unmistakable. Inflation is entrenched. Policy credibility is damaged. And the tools that once maintained stability are no longer sufficient.

Where This Leads

The story does not end in 1978. It culminates in the drastic measures of Paul Volcker, who restores discipline at the cost of severe economic contraction. But that resolution only makes sense in light of what came before.

This post sets the stage. The deeper analysis—of how and why this transition occurred—lies in the individual studies of Martin, Burns, and Connally. Each operates within the same system, but from a different vantage point. Together, they reveal how a structure built to control inflation gradually lost that ability, and how the consequences unfolded across an entire decade.