Astrology of the Federal Reserve: 1934-1948

From balanced budgets to controlled reflation

From “Balance the Budgets of the World!” to “Logical Radicalism”

The intellectual battle that would define American economic policy during the Great Depression did not begin with legislation, nor with the appointment of Marriner Eccles. It began in testimony.

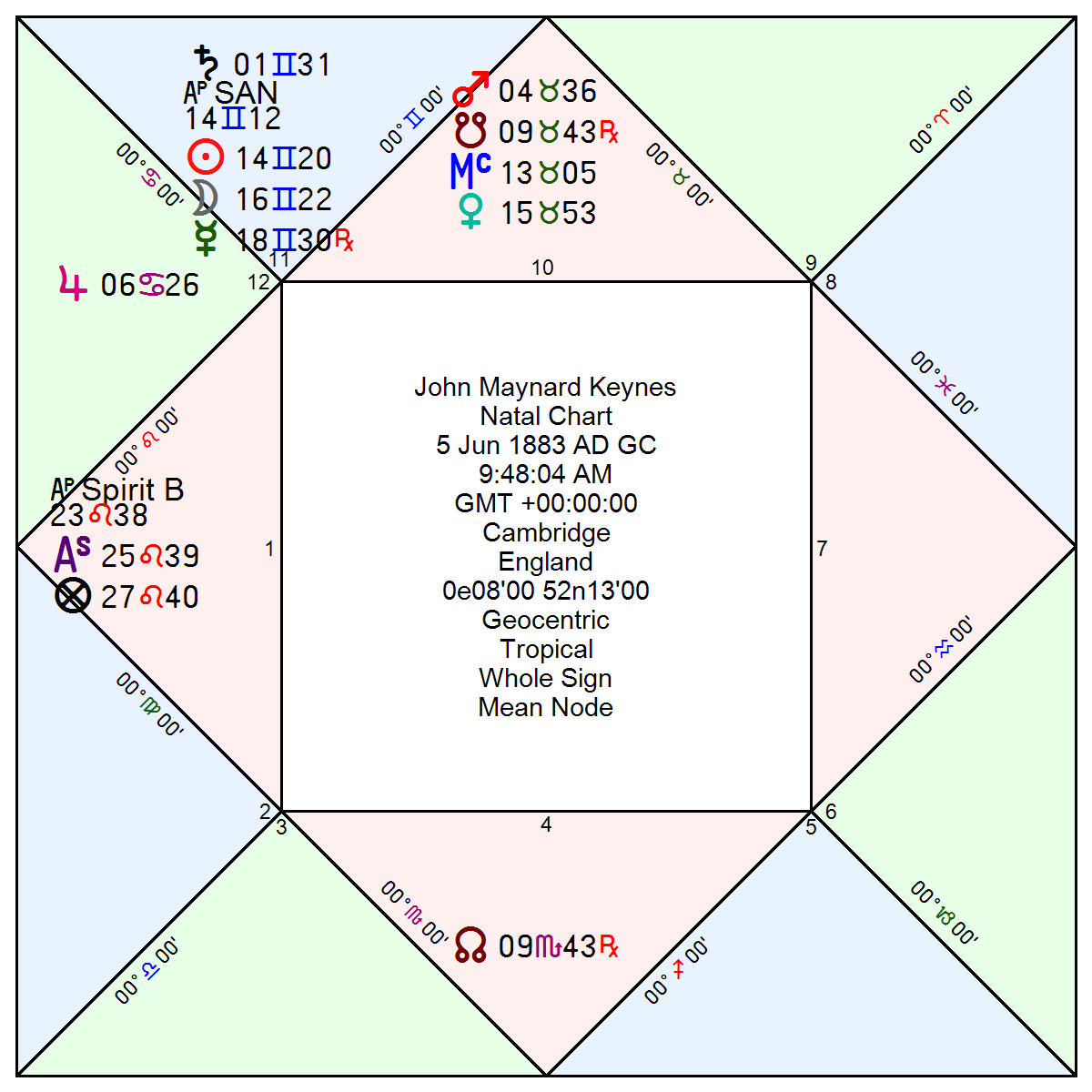

In February 1933, as the financial system teetered on collapse, the United States Senate Finance Committee convened hearings to consider remedies. The first voice the Committee heard was Bernard Baruch, who urged nothing less than a global standard of discipline: “Balance the Budgets of the World!”

Baruch’s position was not extreme—it was orthodox. It reflected a financial worldview shared by figures such as Andrew Mellon, whose earlier call to “liquidate labor, liquidate stocks, liquidate the farmers” expressed the same underlying logic. Economic downturns were not failures requiring intervention, but necessary purges of prior excess. Balanced budgets were not merely prudent—they were restorative.

In astrological terms, this doctrine reflects a Saturnian logic of contraction and discipline. Baruch’s Saturn in Sagittarius retrograde—functioning as Saturn in Gemini—mirrors Mellon’s Saturn in Gemini: regulatory, corrective, and skeptical of expansion. Both men saw contraction as a cleansing force, not a condition to be offset.

Into this consensus stepped an outlier.

On February 24, 1933, Marriner Eccles appeared before the same Committee and delivered testimony that reversed the prevailing logic. The Depression, he argued, was not the result of excess requiring liquidation, but of insufficient demand requiring expansion. His proposed remedy—what he termed “logical radicalism”—was deficit-financed government spending to restore income, prices, and employment.

This was more than disagreement. It was a reversal of causality. Where Baruch and Mellon saw contraction as corrective, Eccles saw it as self-reinforcing collapse.

His remarks were so far outside the mainstream that Rexford Tugwell sought him out after the hearing. Tugwell would later introduce Eccles to Franklin D. Roosevelt, but that moment still lay a year ahead. On the very day of Eccles’s testimony, Roosevelt elevated a pro–balanced budget appointee, and weeks later, on March 10, 1933, delivered a budget-balancing message himself—one Eccles believed would fail. Disillusioned, Eccles returned to Utah.

Eccles Returns—and Rebuilds the System

By 1934, the intellectual tide began to shift. Eccles returned to Washington, first within the Treasury under Henry Morgenthau Jr., where he helped oversee the National Housing Act of 1934. The creation of the Federal Housing Administration was not incidental policy—it was a direct application of his theory: government-backed credit would revive housing, housing would generate employment, and employment would restore income.

Soon after, Eccles accepted Roosevelt’s request to lead the Federal Reserve, replacing Eugene Black. He did so on one condition: the Federal Reserve would have to be restructured. The result was the Banking Act of 1935, passed over the objections of Carter Glass, which centralized authority in Washington and created the institutional machinery for coordinated policy.

With this structure in place, Eccles ensured that monetary policy would not obstruct fiscal expansion. The Federal Reserve maintained low interest rates and stable Treasury borrowing costs, allowing deficits to proceed without being choked off by rising yields. His goal was not uncontrolled inflation, but reflation—a managed rise in prices to counteract the deflation that had hollowed out the economy.

Monetary policy, in Eccles’s system, was no longer primary—it was supportive.

The Philosophy of Expansion—and Its Opponent

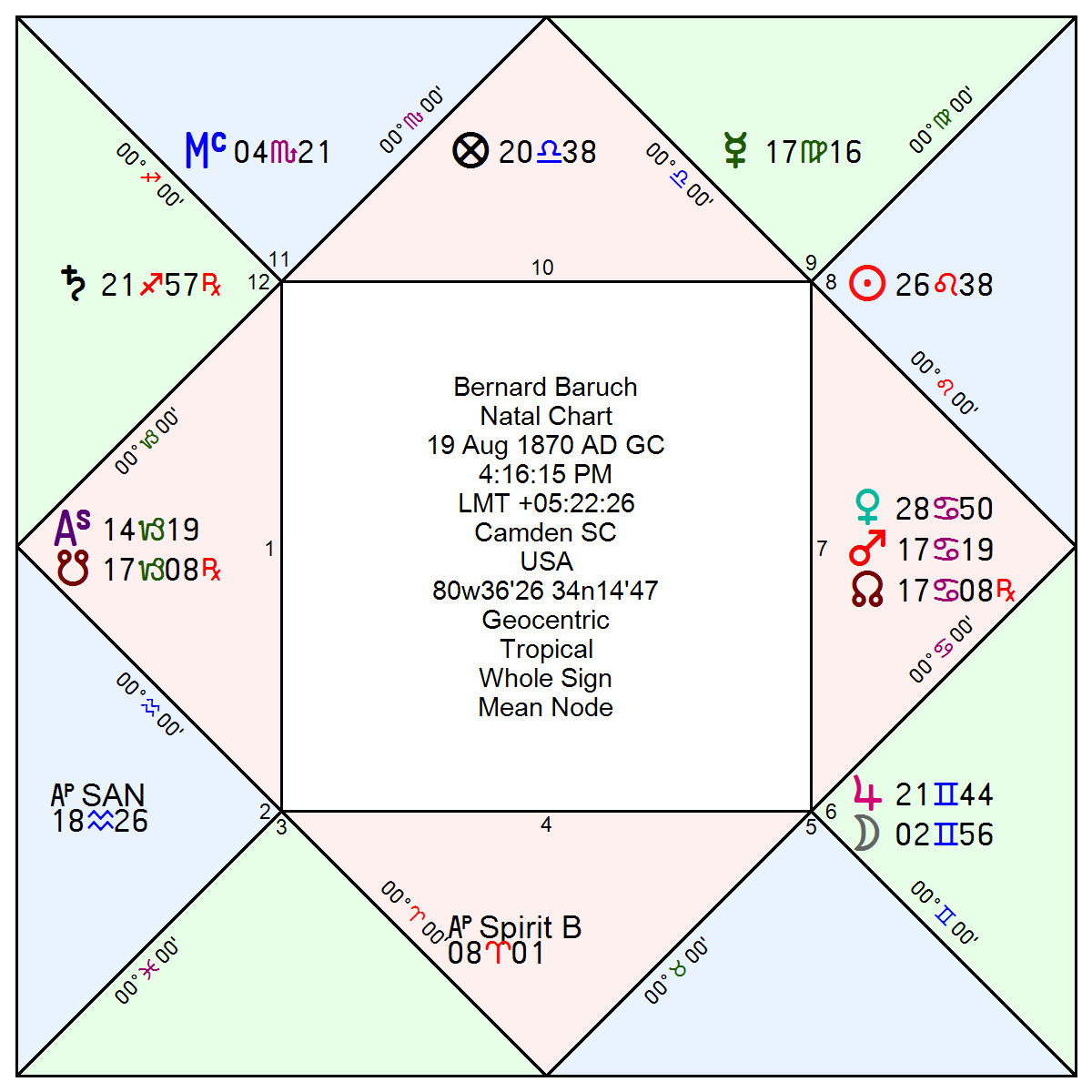

Eccles’s framework is mirrored in his natal chart. With the North Node in Gemini in the 2nd house of wealth, his orientation is toward circulation, exchange, and activity—the very dynamics targeted by fiscal stimulus. His Jupiter in Aquarius retrograde, functioning as Jupiter in Leo, reflects a system in which leadership initiates and private actors respond, generating expansion through the multiplier effect.

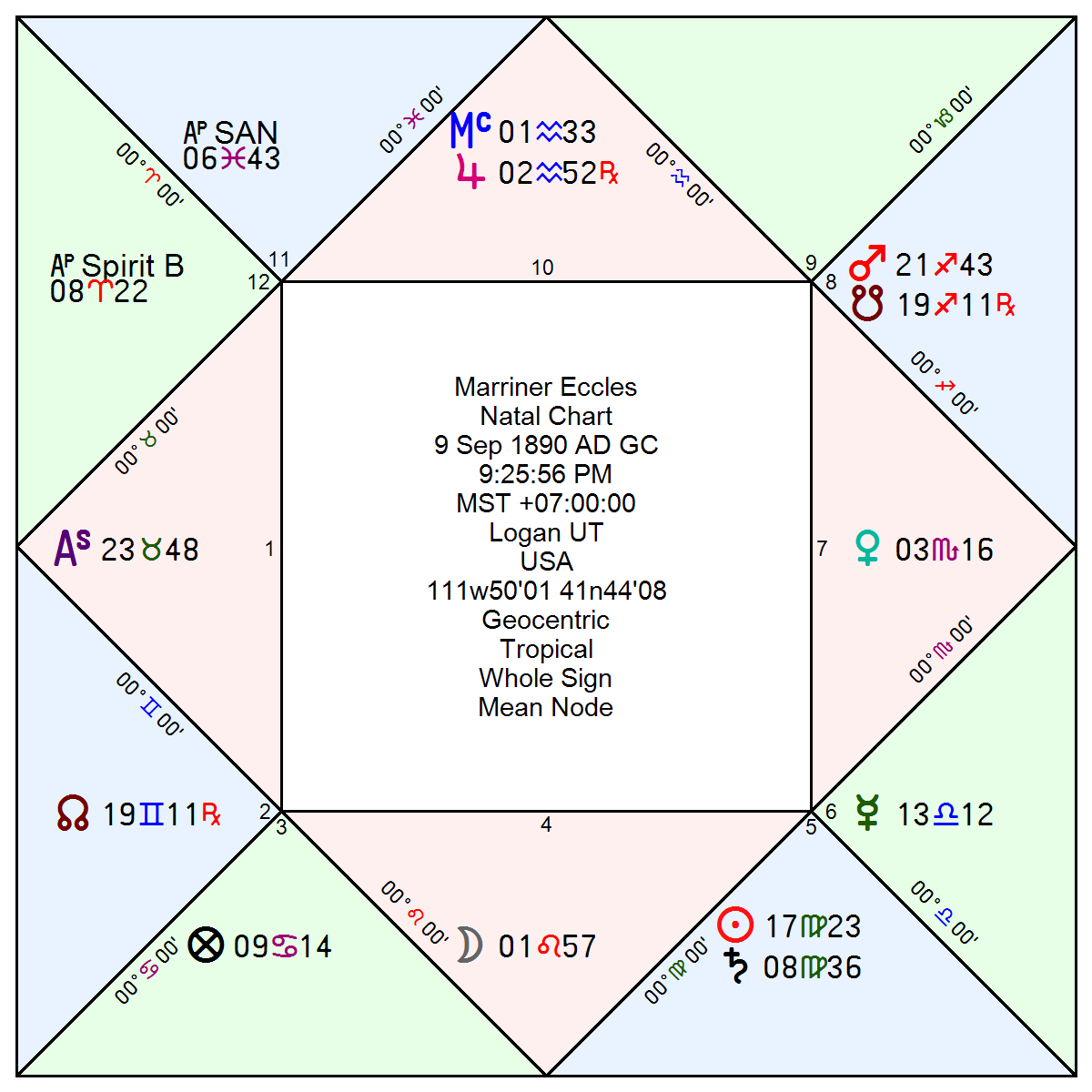

This signature finds a powerful parallel in John Maynard Keynes, whose chart is saturated with Gemini through Saturn, Sun, the Moon and Mercury, listed here in order of degree from lowest to highest. In Keynes, this emphasis on Gemini extends beyond the mechanics of exchange into a full economic philosophy centered on transaction, velocity, and the restoration of activity. But equally important is Saturn in early Gemini, which in his Moon’s configuration signifies contraction preceding expansion. The sequence is critical: downturn first, then restoration of flow. Keynes’s horoscope thus encapsulates the transition from balanced-budget orthodoxy to fiscal stimulus in its purest form.

If Eccles represents the application of this logic within government, Keynes represents its theoretical articulation. Both arrive at the same conclusion: recovery requires not liquidation, but renewed circulation.

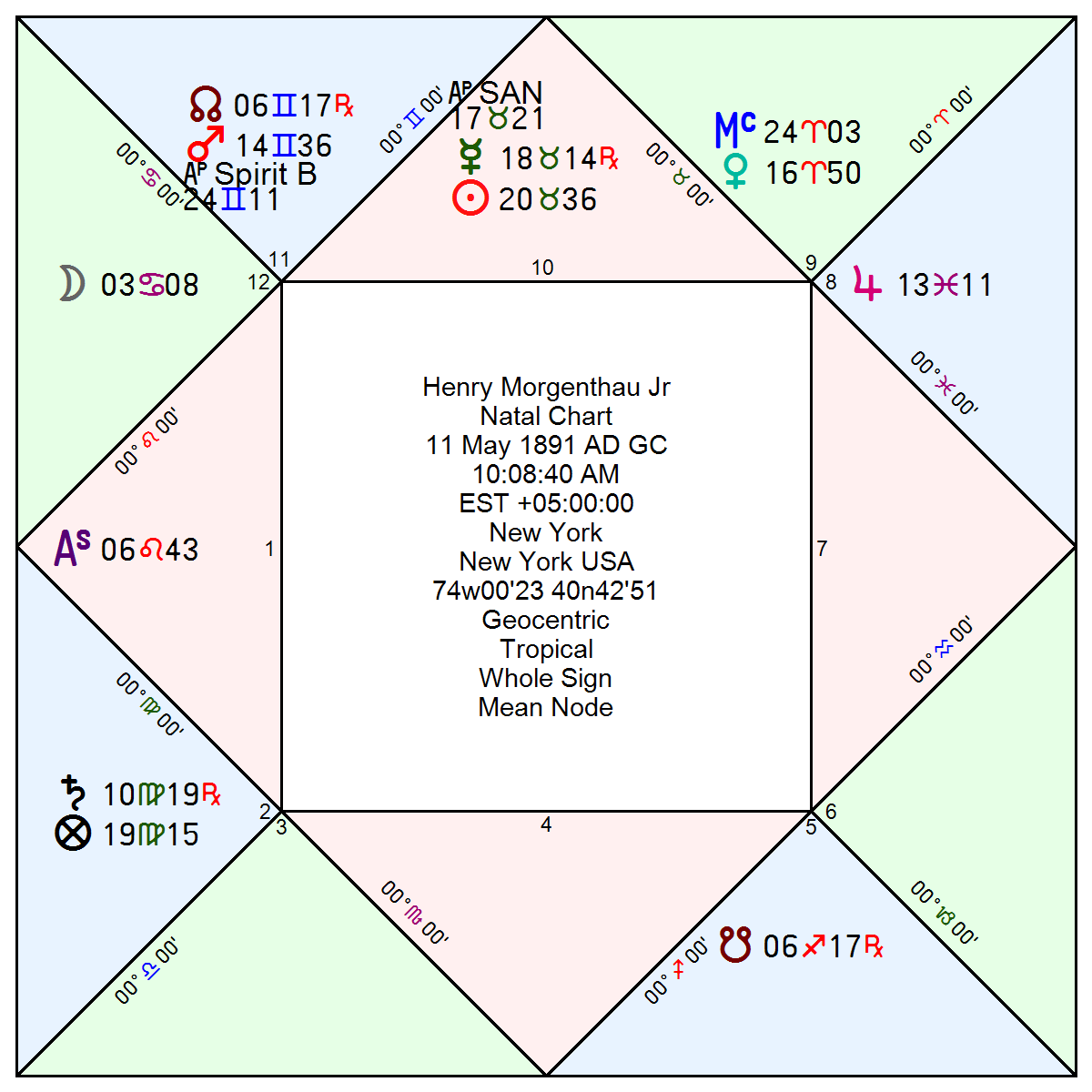

This stands in contrast to Henry Morgenthau Jr., whose preference for balanced budgets reflects a Saturnian emphasis on control and restraint, reinforced by the Lot of Spirit in the bound of Saturn in Gemini. Yet both men share Jupiter as victor, and it is this shared signature that ultimately allows their approaches to converge under different conditions.

War Finance—and the Resolution of the Conflict

With the onset of World War II, the debate between stimulus and discipline was resolved not by theory, but by necessity. Beginning in 1942, the Federal Reserve agreed to peg interest rates on government securities, ensuring that the Treasury could finance the war at low cost.

Under Morgenthau, the Treasury mobilized the public through war bond campaigns—an expression of collective participation consistent with his Jupiter in Pisces. Eccles, for his part, ensured that the financial system could absorb this issuance without disruption by maintaining low rates and stable conditions.

By the early 1940s, fiscal and monetary policy had fused into a single operational system.

The Federal Reserve, once designed as a decentralized rediscounting institution, had become an enabling partner in the financing of the modern state.

The Anomaly of 1937–1938

One episode stands apart. The recession of 1937–1938 represents a rare moment when both frameworks failed simultaneously.

Fiscal policy tightened under pressure for budget balance, while the Federal Reserve raised reserve requirements out of misplaced fears that excess reserves—driven largely by gold inflows—would produce inflation. In reality, the economy remained trapped in a state of weak demand, where liquidity accumulated but was not deployed.

Rather than offsetting each other, these policies reinforced contraction. The result was a sharp downturn that interrupted recovery and exposed the fragility of the system.

It is best understood as an anomaly—a moment when both sides moved in the wrong direction at the same time.

Conclusion

The transformation of the Federal Reserve between 1933 and 1948 was not merely institutional—it was intellectual. The Senate Finance Committee hearings of February 1933 capture this shift in its purest form: from Baruch’s call to balance budgets, to Eccles’s “logical radicalism.”

What followed was not an immediate victory for Keynesian ideas, but a gradual realignment of policy, institutions, and authority. By the early 1940s, the boundaries between fiscal and monetary policy had effectively dissolved, replaced by a coordinated system designed to sustain national economic objectives.

The Federal Reserve did not simply evolve—it was repurposed.

And it all began with testimony.

Now meet the men behind the story.

John Maynard Keynes (1883-1946)